On January 1, 2017, the world changed for credit unions. At least for credit unions serious about Business Banking. In place of a fixed percentage of assets, a cap based on net worth (in other words, tied to the credit union’s ability to absorb lending risk) was implemented. Prior to January 1, NCUA waiver delays resulted in the loss of many good loan deals (and sometimes business clients). In place of the waivers, credit unions now must have sound lending policies, and are judged on how well they follow their policies.

The new NCUA rules create tremendous growth opportunities for credit unions. The best small business clients can contribute 5-10 times the profitability of an individual consumer, and business clients expect to pay extra for time savings and banking advice. However, their decision criteria for selecting a banking partner is different, and requires a radical change in how credit unions think about their service and pricing models. As regulations started to loosen in the late 1990s, credit unions with excess lending capacity saw business loans as a vehicle to produce better returns than they were getting with traditional investments. However, because of the lengthy delays in approvals, and lack of competitive deposit products and merchant services, some credit unions became the “lender of last resort” and many sizeable portfolios were written down or written off altogether when these less desirable, single product borrowers defaulted.

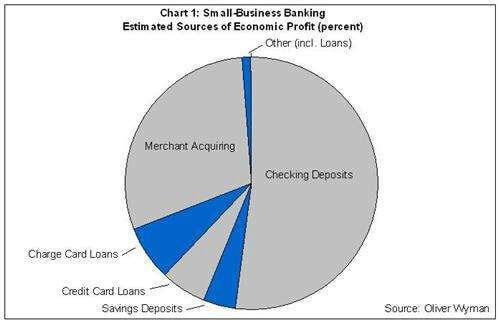

Traditionally, credit union business banking programs have focused primarily on the lending side, but deposits and merchant services account for nearly 80% of small business banking profits, vs only 22% for loans (see chart, Oliver Wyman, 2011). Rates and fee pricing are lower priorities for businesses than having tools to accept payments, access to working capital, ease of making ACH and wire payments, and sound banking advice.

To build a solid, profitable, and sustainable business banking offering, credit unions need to employ people, process, and technology along with competitive products.

Experienced Business Bankers- Forbes describes a small business as “one that does not have a CFO”. This role often belongs to the business owner. A key part of the value of the banking relationship is the ability to get solid financial advice. That takes experienced business bankers. Not just lenders, but staff with experience in deposits, payments, and operations.

Commercial Deposits- Business customers have used community banks or larger banks in the past, and expect a broad variety of deposit offerings. Along with traditional checking, savings, and IRA accounts, they expect their banking partner to offer limits and controls on who can transact business with the CU on behalf of the business client, based on their role with the firm. Banks have offered automated sweeping of excess balances from operating accounts to high-yield accounts for over 20 years. Positive pay (a feature that allows the business to view and approve their checks before they are paid) can help them avoid check fraud losses. And analysis accounts that reward the business client for the overall relationship help attract and retain the most profitable business clients.

Business Services- The most important banking function for many businesses is enabling them to take payments for their products and services. Roughly 30% of small business banking profits are from payments-merchant card payment processing and remote capture and transmission of check images.

Business Online Banking/Mobile/Cash Management- The most valuable commodity for a business owner is time. The right set of capabilities can save your business clients valuable time transacting their banking business, and neutralize the huge brick and mortar advantages of the big banks. Most banks now put the ability to send wires and ACH originations and payments, pay bills and control card limits in their business client’s home office or even in the palm of their hand.

Commercial Lending- Along with more traditional forms of business credit such as term loans, business credit cards and vehicle loans, many businesses need more sophisticated lending products. SBA loans create great value for both clients and the lender, allowing businesses the capital they need to grow and expand, with government guarantees protecting the lender if they default. Loans with variable payment schedules tied to seasonal cash flows, flexible collateral arrangements and commercial construction loans allow the credit union to serve as a “one stop shop” for most of their business clients.

Security- Small businesses are frequently the target of fraud, sometime from their own employees. They expect a banking partner that has the expertise and technology to protect them from cyberattacks, check and payments fraud, and embezzlement.

And finally, speed. Efficient processes and tools for application processing, credit review and funding will help you offer business clients the same amazing service experience credit unions are known for with their consumer members.

Even after credit unions hire experienced business bankers and set up policies and processes, technology often becomes the primary barrier to success. Most credit unions run on core processing systems designed in the 1980s, long before credit unions were allowed to offer business banking. Many offer online banking platforms that serve the needs of consumers well, but lack essential cash management and business functionality.

Credit union IT teams and traditional credit union technology vendors often lack familiarity with business banking, banking regulations and the third-party systems that help serve business banking operations, and their business clients. Choosing the right solutions that will integrate with your current environment and fit your budget can be difficult and risky. A detailed strategy with clear requirements, budgets and timelines will go a long way toward mitigating the risks involved in complex technology decisions.

Enlisting outside advisors with experience in helping credit unions develop and execute the right technology strategy to enable their business services program can go a long way towards minimizing the risk and disruption of a complex technology selection and deployment.

At Arriba Advisors, our partners have over 25 years combined experience in assessing the business banking technology needs of credit unions, and helping them evaluate, select and contract for the right technologies at the right cost of ownership. Feel free to contact us for a free business banking technology market overview.

George McGourty- Originally from Boston and based in Tampa, George has spent his entire 30-year career helping financial institutions evaluate, select, and implement enterprise technologies. He has held senior sales and executive leadership positions with Fiserv, FIS, CSI, Deluxe and Open Solutions as well as co-founding an IT services firm that was later acquired by a Fortune 1000 technology company.

George co-founded Arriba Advisors to help community financial institutions understand and evaluate their technology options, and gain the most value from their technology investments. He is an accomplished negotiator, having personally negotiated over 1,000 technology and services contracts while sitting on the vendor side of the table.

Tom Russell- A native of Miami, Florida, Tom has spent the past twenty years helping financial institutions navigate complex technology and professional services decisions to create efficiencies and gain competitive advantage. Tom has held senior sales roles at TWS Systems, Open Solutions, and Fiserv, managing complex enterprise sales valued up to $25M.

In his role as co-founder and partner at Arriba Advisors, Tom helps our clients understand the technology options available in the market, and how to match their needs and budget to secure the right solution at the right cost of ownership, while identifying and managing the risks inherent in a complex technology purchase.