What are technology gaps? HR sends an email to a new hire Gmail account who’s not yet on-board. In the email are attachments that need to be completed, signed and returned before his first day of work. The email goes to the new hire’s spam folder, that’s a technology gap.

A technology gap is where your manual business processes and loosely coupled technology creates a gap between work steps. Work that needs to get done doesn’t get done. In-between all of the steps, where one task ends and another starts is where can get lost.

These technology gaps exist because there is no one system managing all the work steps in a process. One step could be a manual step, another step may use email, another step could use Salesforce, another step uses a spreadsheet, and another uses PDF forms.

Manual inefficiencies happen when you have too many manual steps with different technologies or no technologies, for example, you are emailed a PDF form to fill out, sign and return. You have to fill it out, print it, manually sign it, scan it in and then email it back. Technology inefficiencies happen when too much technology or too difficult to use technology to accomplish a simple task.

Technology gaps go unnoticed because there is no system making sure work gets done. Using a system like Identifi to control the entire process makes it possible, so nothing falls into technology gaps.

With a system managing all the steps, all work gets completed, gaps cease to exist. It’s a good feeling when you know customers, prospects, vendors, and employees won’t be upset because something vital to them didn’t get done. Then you think about it, and wonder are all the steps getting done efficiently? Do you have manual inefficiencies or technology inefficiencies getting in your way? Since the system gathers data and provides reports online for every step in the process, we have information that can tell us which steps have inefficiencies. The data will tell us which work steps in the process are slowing down sales, customers, employees or vendors. We will have information to compare employee performances to others to identify those who need more training or recognize which steps have too high of a learning curve.

Using the strengths of the system and the strengths of the people together create the most accurate and efficient processes.

1. People are better at solving problems where rules don’t exist, and systems are better where rules are defined. Your process is a known set of business rules, and the system is better at managing the entire process. Each step in the process represents different work to be performed; some work steps are clearly defined, like ordering a background check and making sure it gets done, and the system can achieve this better. Other steps like collaborating with a customer on design are better if done by a person.

2. People are better at dealing with unexpected results, where systems are better when results are predictable. A customer service person is better at dealing with a customer when the customer's three-year-old child has a meltdown. Systems are better at dealing with items that have a defined timeframe to be finished and what to do when it does not get done.

3. People are better at tasks in 3-D, like cooking, cleaning, and driving, all lower-skilled jobs. People are also better at complex mental jobs, highly skilled jobs, like surgery. Today you may question if a person is better at driving than a system. In the definition of better, if we include costs, then people are better at 3-D lower skilled jobs. Sure a system may soon be able to drive better, however at what cost. Vast amounts of money have already gone to driverless research and development, and a lot more money will be needed before we have systems capable of doing all the driving. It is not possible for most companies today to spend the research and development necessary to replace all 3-D low skilled jobs. Despite what we read, artificial intelligence is not going to replace all jobs anytime soon.

4. People are better at being Human, showing empathy, creativity, making people laugh, the human touch is essential and at least for some time will not be duplicated.

Benetrends Financial implemented Identifi’s Business Process Automation and Document Imaging system for their new client onboarding. They were able to eliminate the emailing of PDF forms, clients filling out PDF's, manually signing documents and returning them via scanning or the post office. With Business Process Automation they were able to convert all the forms to online web forms, add online electronic signatures, integrate their CRM data to the Business Process Automation and allow the client to do everything on a smartphone, tablet or PC while gathering data on the overall process performance.

Tim Jagodzinski is the VP of Business Development at Identifi with 28 years working with Business Process Automation and Document Imaging. tjagodzinski@identifi.net

Identifi is very pleased to announce our partnership with Safety Harbor CoderDojo. CoderDojo is a worldwide movement of free, volunteer-led, community-based programming clubs for kids 7 to 17. The CoderDojo concept began in Ireland in 2011 and has since expanded to 1,100 Dojos in 63 countries.

When we first heard about CoderDojo, we knew it was something we wanted to get involved with. We were pleasantly surprised to find that there was already an active Dojo in our own backyard! The Safety Harbor CoderDojo was started in 2015 by Dojo Champions Nancy Vellucci and Anastasia Underwood. Identifi Senior Vice President of Software and Solutions, Aaron Stine reached out to Nancy and Anastasia to see if we could work together. There was an immediate connection and we started collaborating in October of last year.

Since then, we’ve worked together to provide the resources the Dojo needs to be successful. In addition to financial support, Identifi staff also volunteer their time as mentors in the program. That’s been instrumental in expanding the scope of the technology available to learn as well helping each Dojo session run more smoothly.

One of the great things about CoderDojo is how it flips the classroom concept. There’s no lecturing or traditional teaching. Instead, Ninjas (students) learn on their own as well as from each other. We provide resource cards called “Sushi cards” that they can use to learn new skills. Ninjas work at their own pace to create their code projects. We reinforce peer learning with “Team Tickets”. Ninjas can earn a Team Ticket whenever they help out another Ninja. Team tickets are required to complete projects so everyone is motivated to help!

Ninjas earn achievements in the form of belts and badges each time they complete a project. They earn colored belt pins just like a regular Dojo.

They also receive a badge that represents the coding language they used to earn their belt. Ninjas can display their belts and badges by pinning them to their lanyard and wearing them at the Dojo.

As they advance, Ninjas are required to create projects that contribute to the “social good”. For example, they can create a new website that benefits the local community or create an app that helps their school. This reinforces the practical benefits that can come from technology.

We’re thrilled to be supporting the growth of kids in the Tampa Bay Area. Every Ninja in the Dojo will gain a better understanding of the technology that’s driving our world. And for some, CoderDojo may be an avenue to a software or engineering job in the future!

We’re enjoying the ability to give back to the community that has supported us and could not be happier with our combined success!

On January 1, 2017, the world changed for credit unions. At least for credit unions serious about Business Banking. In place of a fixed percentage of assets, a cap based on net worth (in other words, tied to the credit union’s ability to absorb lending risk) was implemented. Prior to January 1, NCUA waiver delays resulted in the loss of many good loan deals (and sometimes business clients). In place of the waivers, credit unions now must have sound lending policies, and are judged on how well they follow their policies.

The new NCUA rules create tremendous growth opportunities for credit unions. The best small business clients can contribute 5-10 times the profitability of an individual consumer, and business clients expect to pay extra for time savings and banking advice. However, their decision criteria for selecting a banking partner is different, and requires a radical change in how credit unions think about their service and pricing models. As regulations started to loosen in the late 1990s, credit unions with excess lending capacity saw business loans as a vehicle to produce better returns than they were getting with traditional investments. However, because of the lengthy delays in approvals, and lack of competitive deposit products and merchant services, some credit unions became the “lender of last resort” and many sizeable portfolios were written down or written off altogether when these less desirable, single product borrowers defaulted.

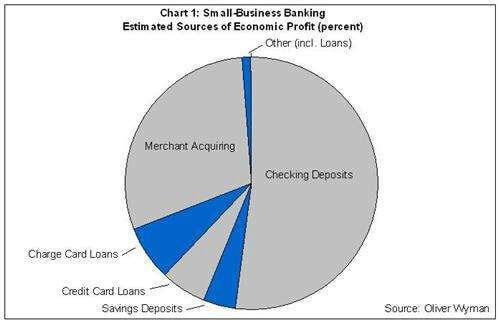

Traditionally, credit union business banking programs have focused primarily on the lending side, but deposits and merchant services account for nearly 80% of small business banking profits, vs only 22% for loans (see chart, Oliver Wyman, 2011). Rates and fee pricing are lower priorities for businesses than having tools to accept payments, access to working capital, ease of making ACH and wire payments, and sound banking advice.

To build a solid, profitable, and sustainable business banking offering, credit unions need to employ people, process, and technology along with competitive products.

Experienced Business Bankers- Forbes describes a small business as “one that does not have a CFO”. This role often belongs to the business owner. A key part of the value of the banking relationship is the ability to get solid financial advice. That takes experienced business bankers. Not just lenders, but staff with experience in deposits, payments, and operations.

Commercial Deposits- Business customers have used community banks or larger banks in the past, and expect a broad variety of deposit offerings. Along with traditional checking, savings, and IRA accounts, they expect their banking partner to offer limits and controls on who can transact business with the CU on behalf of the business client, based on their role with the firm. Banks have offered automated sweeping of excess balances from operating accounts to high-yield accounts for over 20 years. Positive pay (a feature that allows the business to view and approve their checks before they are paid) can help them avoid check fraud losses. And analysis accounts that reward the business client for the overall relationship help attract and retain the most profitable business clients.

Business Services- The most important banking function for many businesses is enabling them to take payments for their products and services. Roughly 30% of small business banking profits are from payments-merchant card payment processing and remote capture and transmission of check images.

Business Online Banking/Mobile/Cash Management- The most valuable commodity for a business owner is time. The right set of capabilities can save your business clients valuable time transacting their banking business, and neutralize the huge brick and mortar advantages of the big banks. Most banks now put the ability to send wires and ACH originations and payments, pay bills and control card limits in their business client’s home office or even in the palm of their hand.

Commercial Lending- Along with more traditional forms of business credit such as term loans, business credit cards and vehicle loans, many businesses need more sophisticated lending products. SBA loans create great value for both clients and the lender, allowing businesses the capital they need to grow and expand, with government guarantees protecting the lender if they default. Loans with variable payment schedules tied to seasonal cash flows, flexible collateral arrangements and commercial construction loans allow the credit union to serve as a “one stop shop” for most of their business clients.

Security- Small businesses are frequently the target of fraud, sometime from their own employees. They expect a banking partner that has the expertise and technology to protect them from cyberattacks, check and payments fraud, and embezzlement.

And finally, speed. Efficient processes and tools for application processing, credit review and funding will help you offer business clients the same amazing service experience credit unions are known for with their consumer members.

Even after credit unions hire experienced business bankers and set up policies and processes, technology often becomes the primary barrier to success. Most credit unions run on core processing systems designed in the 1980s, long before credit unions were allowed to offer business banking. Many offer online banking platforms that serve the needs of consumers well, but lack essential cash management and business functionality.

Credit union IT teams and traditional credit union technology vendors often lack familiarity with business banking, banking regulations and the third-party systems that help serve business banking operations, and their business clients. Choosing the right solutions that will integrate with your current environment and fit your budget can be difficult and risky. A detailed strategy with clear requirements, budgets and timelines will go a long way toward mitigating the risks involved in complex technology decisions.

Enlisting outside advisors with experience in helping credit unions develop and execute the right technology strategy to enable their business services program can go a long way towards minimizing the risk and disruption of a complex technology selection and deployment.

At Arriba Advisors, our partners have over 25 years combined experience in assessing the business banking technology needs of credit unions, and helping them evaluate, select and contract for the right technologies at the right cost of ownership. Feel free to contact us for a free business banking technology market overview.

George McGourty- Originally from Boston and based in Tampa, George has spent his entire 30-year career helping financial institutions evaluate, select, and implement enterprise technologies. He has held senior sales and executive leadership positions with Fiserv, FIS, CSI, Deluxe and Open Solutions as well as co-founding an IT services firm that was later acquired by a Fortune 1000 technology company.

George co-founded Arriba Advisors to help community financial institutions understand and evaluate their technology options, and gain the most value from their technology investments. He is an accomplished negotiator, having personally negotiated over 1,000 technology and services contracts while sitting on the vendor side of the table.

Tom Russell- A native of Miami, Florida, Tom has spent the past twenty years helping financial institutions navigate complex technology and professional services decisions to create efficiencies and gain competitive advantage. Tom has held senior sales roles at TWS Systems, Open Solutions, and Fiserv, managing complex enterprise sales valued up to $25M.

In his role as co-founder and partner at Arriba Advisors, Tom helps our clients understand the technology options available in the market, and how to match their needs and budget to secure the right solution at the right cost of ownership, while identifying and managing the risks inherent in a complex technology purchase.

Back by popular demand…

Back by popular demand…

Integra Client Conference & Training Seminar 2016

Costs:

Full Conference: $249 per Institution

Events Only (Perfect For Guest): $99

More to follow as the dates approach...

We couldn't do it without you! We're celebrating the Holidays with Santa, as another successful year, 2014 comes to a close. We are reminded once again, our greatest achievement is the relationships we have developed over the years with you, our customers, our partners, our employees and our friends, of which most are synonymous. Thank you!

Please enjoy a relaxing, peaceful and safe holiday season and don't forget to celebrate like Santa!

Seasons Greetings from Integra Business Systems, Inc.

Integra Business Systems, Inc. Professional Services Group (PSG) teamed up with the Support Group (SG) to challenge a team made up of the Development Group (DG) and last but not least, a team made up of the Implementation Group (IG) to participate in a canned/boxed good sculpture challenge.

The challenge was created by Christie Russell, Manager of the Professional Services Group to help support an upcoming event by the Feed the Bay Charitable Foundation, of which she is actively involved.

The Feed the Bay 2014 Event is coming on 3/23. This event is used to stock up on food for many homeless and food pantry organizations around the Tampa Bay area.

The challenge to Integra employees to bring some canned goods and then each team prepared a sculpture with the canned goods received. The sculptures were built in the offices of the various teams and are pictured here.

Sculptures needed to be completed by 1 PM on March 21st and were to be delivered to Feed the Bay on March 23rd.

Dolly has escaped her captor(s)? and has been seen partying with known revelers in MA recently. It remains uncertain how Dolly managed to escape. With some degree of certainty we can report Dolly has been receiving daily massages and Botox injections which has produced some amazing results best described as artificial inflation. Dolly was last reported to be seen heading south...

Dolly has escaped her captor(s)? and has been seen partying with known revelers in MA recently. It remains uncertain how Dolly managed to escape. With some degree of certainty we can report Dolly has been receiving daily massages and Botox injections which has produced some amazing results best described as artificial inflation. Dolly was last reported to be seen heading south...

Recently, we asked Dolly's kidnappers for the terms of her release and return safely to Integra. It turns out Dolly has some terms of her own. It seems though her kidnappers, too, are concerned about her getting plenty of attention and exposure to world travels. Our designated world traveler, Abby would probably be willing to take Dolly with her on her travels. Abby's been to Cancun, Costa Rica, Puerto Rico, Ireland, Scotland, France, Australia and New Zealand. She is planning trips to South America and St. Lucia. Dolly could certainly enjoy some spectacular sites. The only problem would be whether Abby had room for Dolly among all her other stuff including dancing shoes, rubber duckie, People magazines, unopened workout videos, hotel property to include towels, lotions, cue tips, mouthwash, pens, and stationary...

I think I really just want to return to FL. At least for awhile. I am not demanding anything much just some time with you all, my adopted family. I am not sure if you heard about the death of my grandmother' and namesake's father recently. It made me very sad. (see below). So I was named after Dolly Parton too!

If I can find a way back to Integra, will someone there be able to take me with them when they go on trips? I really do enjoy that, and have been doing that with the people I stay with. Yes, the actual travel is awkward, folded and sometimes pulled at when in a suitcase by what is called a TSA agent. But I did find my real sister in New Orleans during one of those trips, and met a very nice companion, Ziggy. Did you get my other photos?

I have heard of something called C.O.D., maybe I can use that to return, would that be OK? Us sheep are not good with initials after BaaBaa.

Yours truly, Dolly

LONDON -- Keith Campbell, a prominent biologist who worked on cloning Dolly the sheep, has died at 58, the University of Nottingham said Thursday. Campbell, who had worked on animal improvement and cloning since 1999, died Oct. 5, university spokesman Tim Utton said. He did not specify the cause, only saying that Campbell had worked at the university until his death. Campbell began researching animal cloning at the Roslin Institute near Edinburgh in 1991. The experiments led to the birth in 1996 of Dolly the sheep, the first mammal to be cloned from an adult cell. The sheep was named after singer Dolly Parton. Researchers at the time said that the sheep was created from a mammary gland cell, and that Parton offered an excellent example.